In critical raw materials, the pressure is no longer abstract. In recent procurement cycles, I have seen battery and magnet projects stall because a single licensed Chinese component could not ship, while EU projects that met every technical requirement still waited on permits. Board-level risk committees have started asking blunt questions: not about margin, but about whether gigafactories, fabs, and defense programs can be built and kept running under two incompatible regulatory logics. That is the backdrop for looking at the EU’s Critical Raw Materials Act (CRMA) and China’s export control regime as a single, colliding system rather than two parallel policies.

The incidents that shaped this view are concrete: the 2010 rare earths dispute that exposed how quickly a choke point can be weaponised; the 2022-2023 European energy shock that demonstrated what regulatory delay can do to industrial output; and, more recently, Chinese licensing frictions around gallium, germanium and graphite that rippled through EV and semiconductor sourcing. Each time, the lesson was the same: formal legality and commercial logic matter less than physical ability to move atoms and equipment on time.

Key Points (Non-Exhaustive)

- The EU CRMA is a supply-side framework with quantitative 2030 targets (extraction, processing, recycling) and legally binding permitting timelines for designated “Strategic Projects”.

- China’s critical materials export controls are primarily demand-side and licensing-based, combining military end-use prohibitions, end-user verification and, in some cases, technology and equipment controls with extraterritorial effects.

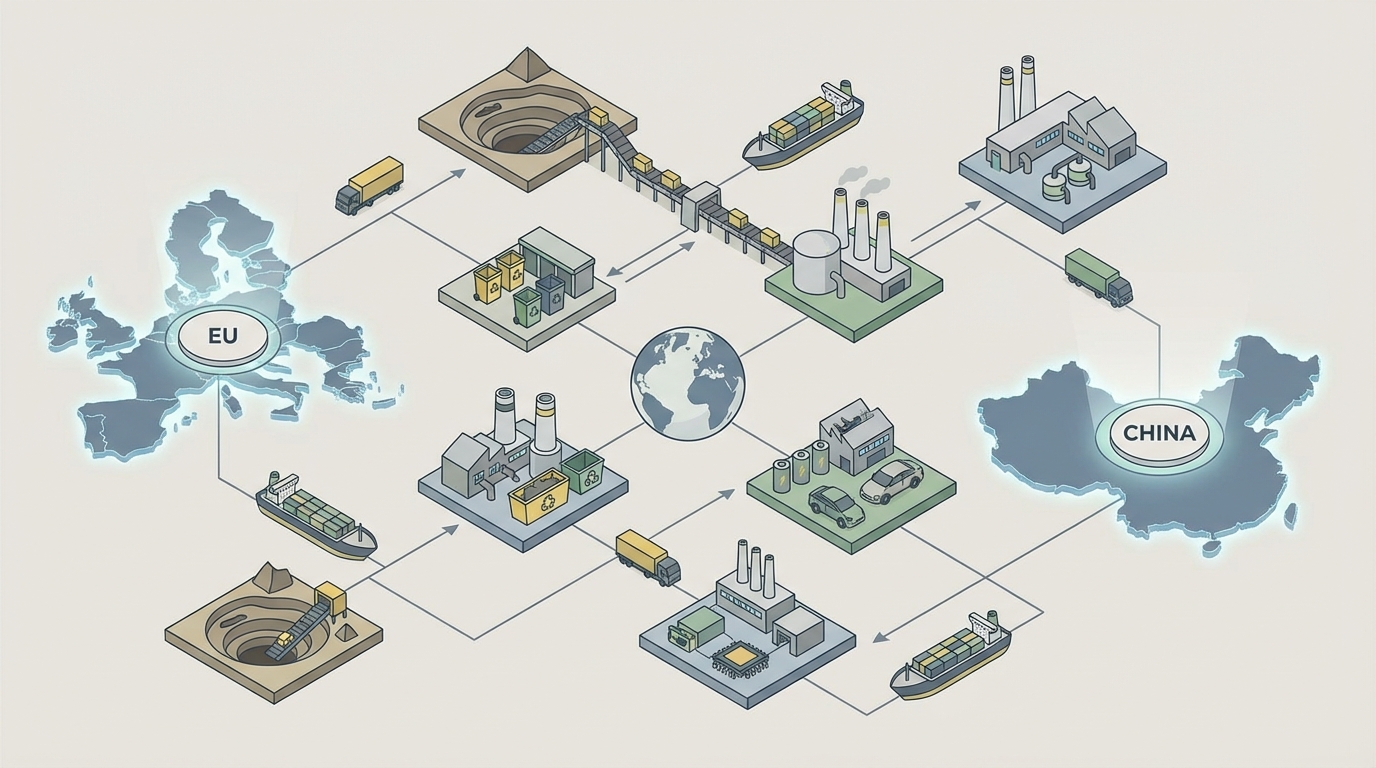

- The two regimes intersect in batteries, semiconductors and defense supply chains, where CRMA-driven diversification projects depend on processing equipment and know-how that Chinese measures can delay or restrict.

- According to the input materials, 2025-2026 policy steps (additional Chinese measures and partial suspensions, plus an expanded list of EU Strategic Projects) create a narrow and uncertain window in which both sets of rules evolve at once.

- Operationally, the main friction does not lie only in ore availability but in licensing timelines, documentation burdens and equipment dependencies that can slow commissioning even when funding and political support are in place.

FACTS

EU Critical Raw Materials Act (CRMA): Objectives and Targets

The EU Critical Raw Materials Act (CRMA) is an EU legislative framework designed to strengthen the security and resilience of the Union’s supply of critical and strategic raw materials. The final text, as adopted in 2024, sets quantitative benchmarks for 2030, including:

- a share of at least 10% of the Union’s annual consumption of strategic raw materials originating from extraction within the EU,

- a share of at least 40% of annual consumption from processing within the EU,

- a share of at least 25% of annual consumption from recycling within the EU, and

- a limit whereby not more than 65% of the Union’s annual consumption of each strategic raw material at any relevant stage of processing should come from a single third country.

These benchmarks are framed as Union-wide targets and are accompanied by monitoring and reporting obligations. The CRMA distinguishes between “critical raw materials” and a narrower list of “strategic raw materials”, the latter associated with applications such as batteries, permanent magnets, semiconductors, aerospace and defence.

CRMA Permitting and Strategic Projects

A core operational feature of the CRMA is the introduction of accelerated permitting for designated “Strategic Projects”. The Regulation requires Member States to respect maximum timelines for permitting decisions:

- for extraction projects classified as Strategic Projects, the overall permit-granting process is capped at 27 months from the date of valid application,

- for processing and recycling Strategic Projects, the corresponding cap is 15 months.

Member States are obliged by the CRMA to establish a single national “one-stop shop” (Single Point of Contact) to coordinate permitting procedures for Strategic Projects. The European Commission, assisted by a Board composed of Member State representatives, is tasked with selecting Strategic Projects based on criteria such as strategic importance, technical feasibility, environmental and social standards, and contribution to Union targets.

The input materials refer to Commission communications indicating that, by December 2025, around 60 Strategic Projects had been approved, including a subset in third countries, with European Investment Bank (EIB) and European Bank for Reconstruction and Development (EBRD) financing linked to delivering volumes to the EU market. These developments are part of the scenario described in the supplied sources and go beyond what is directly embedded in my training data.

In addition, broader EU economic security initiatives require large companies in certain sectors to conduct supply chain risk assessments, including mapping dependencies on single-country suppliers for critical materials and technologies. These risk assessments interact with CRMA objectives but are established in separate policy instruments.

Baseline: Chinese Export Controls on Critical Materials up to 2024

China has a long-standing framework for controlling the export of strategically sensitive goods, implemented through the Export Control Law, the Foreign Trade Law and implementing regulations administered primarily by the Ministry of Commerce (MOFCOM) and other agencies.

In 2023-2024, a series of measures brought several critical materials and related technologies under tighter licensing:

- gallium and germanium-related items were added to export control catalogues, requiring exporters to obtain case-by-case licences, with end-use and end-user review,

- certain rare earth permanent magnet manufacturing technologies and know-how were placed under export licensing, reflecting concern about military and high-tech applications,

- from late 2023, several forms of graphite products became subject to export licensing, with intended justifications including “national security” and “environmental” grounds.

These measures typically involve requirements for exporters to submit detailed documentation: end-use certificates, end-user declarations, information on intermediaries, and in some cases proof that the transaction does not involve military or weapons-of-mass-destruction end uses. Chinese authorities maintain discretion to deny or delay licences. Official communications have framed these controls as consistent with World Trade Organization (WTO) rules, often citing environmental protection or national security as legal bases.

China also maintains a catalogue of technologies subject to export restrictions, which goes beyond physical commodities to cover equipment designs, process technology and software. For critical raw materials, this can include processing and recycling technologies, as well as manufacturing equipment for battery materials and permanent magnets.

Reported 2025–2026 Developments in Chinese Controls

The article and source list provided for this briefing describe additional Chinese measures in 2025–2026 that fall outside the direct scope of my October 2024 training cut-off. The key elements, as described in those materials, can be summarised as follows (they are presented here as reported, not independently verified):

- A MOFCOM “Announcement 46” in October 2025 that broadened export controls on graphite, gallium, germanium, certain rare earths, batteries and related processing equipment, reportedly with an explicit reference to extraterritorial reach and strengthened end-user screening.

- A subsequent “Announcement 72” in November 2025 that partially suspended U.S.-specific licensing requirements under Article 2 of Announcement 46, effectively reverting some items to “ordinary” licensing channels for U.S.-destined exports, while maintaining Article 1 prohibitions on military and weapons-related end uses.

- Interpretations in the legal commentary cited in the input that characterise this as a “pause” tactic: retaining the legal architecture for tight controls but easing practical enforcement for some destinations, with the possibility of rapid reinstatement in response to geopolitical developments.

According to these same materials, Chinese export controls in this period also cover certain categories of processing and recycling equipment and associated technology transfers, creating an additional layer of control separate from the export of raw and processed materials themselves.

Interaction Points Identified in the Input Materials

The provided article highlights several interaction points between CRMA implementation and Chinese controls, particularly for batteries, semiconductors, permanent magnets and defense applications:

- CRMA Strategic Projects in extraction and processing (including in third countries) that are aimed at reducing dependence on Chinese refining capacity, especially for lithium, nickel and rare earths.

- Simultaneous dependence of many of these projects on Chinese-origin processing and recycling equipment, technology licences and engineering services, which fall under China’s export control and technology transfer screening regimes.

- Chinese dominance in refined graphite production for battery anodes (commonly estimated in public sources at over 90% of global capacity), juxtaposed with new Chinese export licensing requirements on graphite products.

- Reports in the supplied sources that some external analysts expect certain CRMA-enabled projects, if fully implemented and supplied with necessary equipment, to reduce single-country dependencies by on the order of 30–50% by the end of the decade.

- References to estimated cost impacts and internal Chinese price movements associated with previous rounds of controls, as an illustration of how quickly licensing measures can reshape midstream economics.

These points form the factual backbone for the scenarios developed in the interpretation section below, always subject to the caveat that post-2024 developments are drawn from the user-supplied documentation rather than from the model’s own training data.

INTERPRETATION

Two Regulatory Logics: Supply-Side Acceleration vs Licensing Choke Points

Viewed through a supply chain lens, the CRMA and China’s export controls embody opposite regulatory logics. The CRMA is structured as a positive industrial policy: accelerate domestic and allied capacity by shortening permits, clarifying “Strategic Project” status and linking EU and multilateral funding to projects that deliver into the European market. Chinese measures, in contrast, operate as negative space controls: exports are allowed so long as licences are granted, but the existence of a discretionary licensing tier introduces uncertainty and time risk at the point of shipment or equipment delivery.

In practice, both logics converge on the same assets. A rare earth separation plant in Europe that qualifies as a CRMA Strategic Project might rely on a solvent extraction line, catalyst package or control software that is designed in China and covered by export controls. The CRMA may compress the front-end permitting to 15 months, but if the Chinese exporter faces months of additional scrutiny or a temporary pause on licences, commissioning dates slip. This is the core operational paradox: a policy designed to de-risk dependency can still be bottlenecked by that very dependency at the equipment and technology layer.

From an operational standpoint, this is where I have seen the largest disconnect between boardroom narratives and project reality. Slide decks often celebrate new non-Chinese feedstock sources, while the vendor list for critical process steps still shows single points of failure in equipment and services that are regulated under Chinese law. When export control officers and project engineers only meet after procurement decisions are made, the room for manoeuvre is already narrow.

Batteries and EVs: Graphite, Cathode Materials and Recycling

Battery supply chains sit at the sharpest intersection of CRMA ambitions and Chinese controls. China’s dominant share in refined graphite and key cathode precursor materials gives Beijing substantial leverage through licensing, even without outright bans. CRMA targets encourage more EU-based processing and recycling, and Strategic Projects seek to anchor anode, cathode and active material capacities closer to end-use gigafactories.

that said, as described in the input materials, many planned European and allied recycling lines, high-nickel cathode facilities and synthetic graphite pilots are modelled around Chinese-origin technologies. Where those technologies or associated engineering services are captured by export control catalogues, each new project adds to the licensing pipeline. If, as reported, there is a period in 2025–2026 when some U.S.-focused graphite and gallium controls are partially suspended, this could create a temporary easing of friction for certain destinations. But that kind of “pause window” inherently introduces timing risk: projects that depend on it for commissioning are exposed if controls are reinstated at short notice.

From a supply resilience viewpoint, the binding constraint in the second half of the decade may be less about securing raw ore and more about securing diversified, non-controlled equipment and process routes for refining and recycling. CRMA benchmarks do not in themselves guarantee that those alternative routes will be technically or economically mature in time. Where such routes are not yet available at scale, the EU’s reliance on Chinese technologies effectively caps how fast dependency ratios can fall, regardless of how much political will and funding are mobilised.

Semiconductors, Magnets and Defense: The Military End-Use Firewall

Semiconductor and defense applications add another layer: explicit military end-use restrictions. Chinese export control law, and the specific measures cited in the input, maintain a clear prohibition on supplying controlled items for military or weapons-of-mass-destruction purposes, even where certain commercial flows are temporarily eased.

In practice, this creates a split regime. A rare earth magnet or gallium component for a civilian telecom application might be licensable during a pause, while a similar item integrated into a radar, avionics or missile system remains off-limits. For companies serving dual-use markets, disentangling these flows is extremely complex: the same upstream material may be processed in shared facilities before being allocated across civilian and defense programs.

CRMA Strategic Projects in permanent magnets, rare earths and specialty alloys can, over time, reduce this vulnerability by anchoring more of the value chain inside jurisdictions with aligned security frameworks. But in the interim, any defense-facing program that depends on a Chinese-controlled step is exposed to a binary risk: licences may be refused outright, not merely delayed. That risk is structurally different from the “delay and documentation” friction seen in more civilian segments.

Administrative Friction as a Structural Cost to Supply Security

Another consistent pattern in both regimes is the use of time and paperwork as a policy tool. The CRMA compresses permitting timelines but adds new layers of reporting, environmental and social assessment, and public consultation. Chinese export controls formally allow exports but front-load them with case-by-case review, end-user verification and the possibility of prolonged “under review” status without a clear deadline.

From a supply chain governance perspective, this means that administrative friction becomes a quasi-physical constraint. In projects I have observed, even a three to six month unexpected licensing delay for a single furnace, reactor, or solvent extraction battery can derail integrated commissioning plans, trigger liquidated damages discussions in EPC contracts, and undermine board confidence in entire industrial policy packages.

One could argue that this friction is not a bug but the point: for Beijing, it introduces strategic ambiguity and leverage without resorting to overt embargoes; for Brussels, it is the price of pursuing more stringent environmental and social standards while fast-tracking “strategic” capacity. The operational reality on the ground, however, is that planning horizons compress and risk buffers disappear quickly when both permitting and licensing clocks are running simultaneously.

Three-Way Risk Arbitrage: EU Rules, Chinese Controls and Third-Country Projects

The input article frames corporate decision-making in this space as a three-way arbitrage among EU regulatory incentives, Chinese export controls and the practicalities of third-country project development. In my experience, that framing maps well to how advanced procurement and strategy teams now structure internal discussions, even if they avoid that vocabulary.

On one side are CRMA-aligned projects, including extraction and processing ventures in the EU and friendly jurisdictions, often with public or multilateral financing. These carry permitting risks, community acceptance questions and, in some cases, technology maturity concerns, but they sit within a relatively predictable regulatory narrative. On the other side are existing supply chains anchored in China, where physical capacity and technical performance are proven, yet flows are subject to licensing volatility and geopolitical shocks.

Connecting these two are hybrid structures: joint ventures, tolling agreements and offtakes in countries such as Australia, Canada or certain Southeast Asian states, often using Chinese equipment, engineering or capital. The risk profile of such arrangements is layered: the host country’s permitting, the EU’s CRMA alignment, and Chinese attitudes to outbound investment and technology export. The weakest link often dictates feasibility: for example, a fully permitted graphite project in a third country can still be unbankable if lenders see unresolved exposure to Chinese licensing on key process steps.

Across all three legs, the pattern that worries me most is complacency about “temporary” pauses in controls. Historical experience with rare earths and other strategic commodities suggests that once a licensing architecture is built, it rarely disappears; at most, enforcement intensity oscillates. Treating a period of leniency as a permanent reset, rather than as one point on a policy cycle, has been a recurring failure mode in supplier evaluations I have reviewed.

WHAT TO WATCH

Several categories of signals are likely to be critical for understanding how the CRMA–China interaction evolves in 2025–2026 and beyond:

- CRMA Implementation Pace: Publication of delegated acts, updated lists of strategic raw materials, and actual time-to-permit data for early Strategic Projects, compared with the nominal 27-month and 15-month caps.

- Strategic Project Portfolio: Geographic distribution of approved projects (EU vs third countries), technology choices (Chinese-origin vs alternative process routes), and evidence of bottlenecks in grid access, water, and downstream offtake.

- Chinese Licensing Practice: Not only formal announcements (such as those labelled 46 and 72 in the input) but also anecdotal lead times for export licences on specific HS codes, especially for graphite, rare earth-related materials, and processing equipment.

- Technology Control Expansion: Any moves by China to extend export controls deeper into software, control systems, and engineering services for critical material processing, and any reciprocal measures by the EU or allied countries.

- End-Use and End-User Scrutiny: Shifts in how strictly Chinese authorities enforce military end-use restrictions, and how EU and allied defense programs adjust sourcing strategies for magnets, radar components and other sensitive items.

- Market Behaviour Under Stress: Episodes of extreme lead time elongation, spot availability crunches or sharp shifts in trade flows (for example, sudden growth in intermediary routing through specific hubs) that may indicate underlying licensing tightness before it is fully visible in formal policy.

- Legal and WTO Dynamics: Dispute settlement moves, formal complaints, or negotiated arrangements around critical materials that might stabilise or, conversely, further politicise export control application.

In previous cycles, early signals often surfaced first in the operational sphere: freight forwarders reporting unusual customs holds, smaller suppliers losing access to Chinese-origin inputs without clear explanations, or engineering contractors quietly warning about long replacement times for specific equipment. Formal regulatory texts sometimes lagged behind these practical indicators.

Note on the Ti22 methodology Ti22’s analysis combines close reading of primary regulatory texts (such as the CRMA and Chinese export control announcements) and guidance from relevant authorities with contemporaneous market reporting where available, and a technical breakdown of end-use applications in batteries, semiconductors, magnets and related sectors. The objective is not to forecast prices but to map how legal provisions and technical constraints interact to shape feasible supply chain configurations.

Conclusion

The collision between the EU’s CRMA and China’s export controls is no longer a theoretical scenario; it is increasingly the day-to-day operating environment for those responsible for critical material supply chains. On one side is a rules-based attempt to accelerate domestic and allied capacity through clear timelines and targets; on the other, a flexible, discretionary licensing apparatus that can modulate global flows of materials, equipment and know-how with relatively short notice.

In that environment, the strongest determinant of outcomes is not headline policy rhetoric but the granular interaction between permits, licences, equipment vendors and project critical paths. Projects built on the assumption of frictionless access to controlled Chinese inputs face a structurally different risk profile from those designed around diversified process routes, regardless of where ore is mined. Conversely, CRMA-inspired ambitions can underdeliver if they do not fully confront continuing dependencies at the equipment and technology layer.

As both systems evolve through 2025–2026, the balance of power in critical raw materials will be shaped as much by administrative practice and technical path-dependence as by new legislative texts. Maintaining clarity on mechanisms, scope, and real-world bottlenecks, and sustaining active monitoring of weak regulatory and industrial signals, will be central to understanding how this collision of systems ultimately reshapes the supply chain landscape.

Sources

- EU Critical Raw Materials Act Adopted — European Commission — ec.europa.eu

- EU Approves Critical Raw Materials Act to Cut China Dependence — reuters.com

- China Tightens Export Controls on Graphite Used in EV Batteries — asia.nikkei.com

- China Tightens Export Controls on Graphite Amid Global Supply Chain Concerns — scmp.com

- Beijing Expands Export Controls on Critical Minerals and Technologies — ft.com

- China Expands Export Controls on Rare Earths and Magnet Tech — bloomberg.com

- What the EU’s Critical Raw Materials Act Means for Industry — politico.eu

- China’s New Export Controls to Hit Global Rare Earths Supply — metalbulletin.com

- China Export Controls and EU CRMA: Impact on Battery and Magnet Supply Chains — supplychaindive.com

- How China’s Export Controls Affect EV Battery Sourcing — cbtnews.com