Executive Summary. The Chinese export control regime for gallium (Ga) and germanium (Ge) no longer operates as a hard stop on flows but as an adjustable-intensity mechanism, centered on three levers: (1) the granularity of material specifications and purity thresholds, (2) the classification of end-uses and end-users, and (3) an extraterritorial component based on MOFCOM Announcement 61. Since November 2025, a partial suspension, valid until November 27, 2026, has reopened access to standard licensing channels for U.S. civilian customers, while leaving military red lines intact. In practice, the dynamic is not defined by access to Ga-Ge volumes, but by licensing lead times, cascading traceability, supply chain fragmentation, and regulatory vulnerability looking toward late 2026.

The most structural feature of the system lies in the coexistence of suspensions with distinct timelines: one for restrictions specifically targeting the U.S. on Ga/Ge, and another for announcements extending the extraterritorial scope to products manufactured outside China. This dissociation creates a fragmented compliance window, where flows may appear regularized in the short term while remaining exposed to a regime shift in the medium term. The result is not merely legal; it translates into concrete industrial choices regarding refining localization, supplier qualification, and the configuration of multi-source logistics chains.

I. Control Regime Architecture: Material Scope and Technical Thresholds

A. Controlled Materials and Product Forms

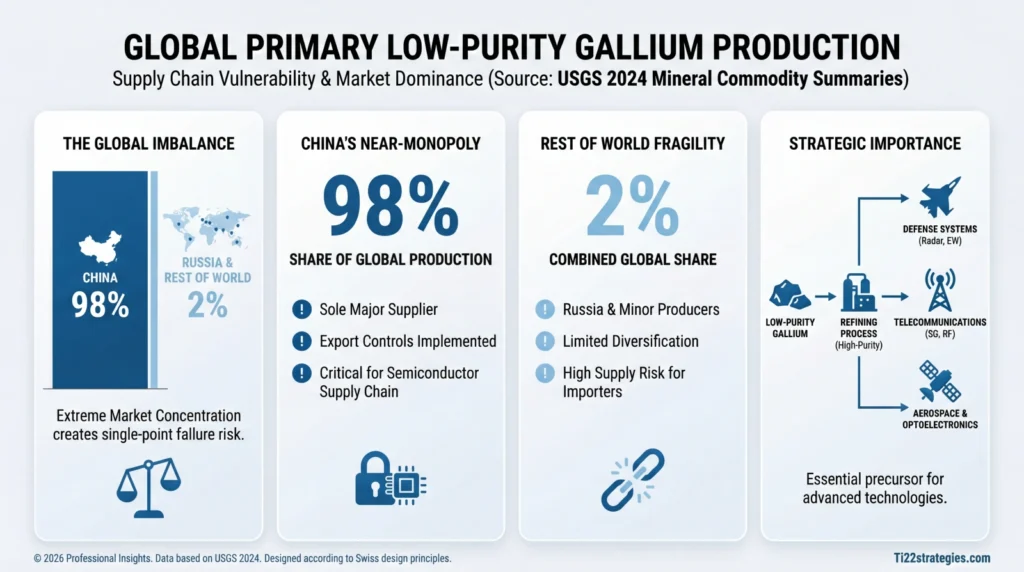

The Chinese framework does not target gallium and germanium as abstract categories, but rather specific product forms and precise purity levels, articulated around strategic uses in optoelectronics and semiconductors. The control texts distinguish between raw metals, value chain intermediates (ingots, powders, compounds), and highly processed forms such as epitaxial wafers. This product-form approach allows for refined licensing selectivity, modulating severity between flows with potential military impact and those oriented toward mass civilian usage.

Gallium. Controls specifically cover pure gallium metal, gallium wafers used in the manufacture of high-frequency devices, and structural compounds such as gallium arsenide (GaAs) and gallium nitride (GaN) [2][6]. These forms are at the heart of 5G, RF power, LED, and advanced photovoltaic value chains. The control texts explicitly cover critical civilian applications, meaning the boundary does not lie between civilian and military, but within civilian segments themselves, depending on the end-user profile.

For gallium, the extraterritorial component is not limited to direct exports from China. It extends to products processed outside China that incorporate Chinese-origin gallium inputs, with no specific de minimis threshold declared for gallium alone, whereas a 0.1% de minimis rule applies to other categories of controlled materials [1][3]. This absence of an explicit threshold for Ga reinforces the potential scope of controls once Announcement 61 is fully in force.

Germanium. Germanium is treated similarly, but with particular emphasis on forms used in optics and infrared detection: raw germanium, ingots, powders, as well as compounds such as germanium dioxide dedicated to optical fibers [6]. These materials supply civilian segments (long-haul optical fibers, infrared optics for industrial imaging) and dual-use segments (defense optronics, night vision systems, guidance). Extraterritorial controls mirror those of gallium: any product manufactured outside China incorporating Chinese-origin germanium inputs or technologies may fall under the scope of MOFCOM licenses [3][5].

A key point for industrial directors is that the material does not cease to be controlled when it changes form: a flow of primary gallium melted into an ingot in a third country and then re-cut into wafers potentially retains the regulatory marking of its Chinese origin. Upstream traceability thus becomes a parameter as critical as purity or electrical characteristics in supplier qualification.

B. End-Use and End-User Rules

Beyond material specifications, the Chinese regime structures a hierarchy of permissiveness based on the end-user profile and the declared usage scenario [1][3]. The architecture of the texts converges toward a logic of structural denial for certain profiles, in-depth filtering for others, and standard treatment for a final circle.

Prohibited End-Users. Foreign military users are targeted for refusal in principle, as are entities listed on China’s export control list or watch list, including their subsidiaries, branches, or entities owned at least 50% [1]. In these cases, the logic is not to examine the transaction on a case-by-case basis, but to structurally block access to Chinese-origin Ga/Ge.

Prohibited End-Uses. The regime also prohibits the supply of Ga/Ge for the design, development, production, or use of weapons of mass destruction and their delivery systems [1], as well as for potential military applications, notably advanced semiconductors capable of powering defense systems [5]. This prohibition field functions as a functional filter: even a civilian user may be refused if the projected use falls into these categories.

U.S. Civilian End-Users. Since November 2025, the mechanism has evolved for this category: U.S. civilian customers once again have access to standard licensing channels [2][3][6]. This means their applications are no longer blocked by a principle-based ban, but processed under the ordinary framework, with evaluation of the dossier, end-use declarations, and user profile. Approvals remain discretionary, however, and the exact criteria for acceptance or refusal are not fully public.

The fundamental pivot lies in the shift from a presumed ban to licensing filtration. In industrial terms, the difference translates not only into the possibility of continuing supply, but into a new category of risks: delays, calendar unpredictability, and the possibility of sudden tightening of license processing without any apparent change in physical volumes available.

C. Extraterritorial Obligations and De Minimis Rules

MOFCOM Announcement 61 introduces an extraterritorial component that constitutes the most structural dimension for Ga-Ge value chains located outside China. It subjects products manufactured in third countries to licensing if they incorporate specified Chinese inputs or technologies, even if the final exporter is not established in China [3][5].

The text covers, notably, rare earth and strategic metal products manufactured outside China when they rely on Chinese technologies in five key steps [5]:

- Mining extraction;

- Smelting and separation;

- Metal smelting;

- Magnet or functional intermediate manufacturing;

- Recycling and recovery of secondary resources.

For gallium and germanium, this logic extends to material flows: a Ga/Ge product manufactured outside China, but containing Chinese-origin inputs, may enter the scope of licenses, with no de minimis threshold explicitly fixed for these two metals [5]. The absence of a quantified threshold intentionally leaves a wide margin of appreciation to the control authority, complicating ex-ante regulatory risk modeling by product or client.

Current Status. As of January 2026, Announcement 61 is suspended until November 10, 2026 [2][3]. Concretely, the extraterritorial obligations it foresees are not applied during this period. However, this suspension does not represent a repeal: the legal framework remains in place and can be reinstated at the end of the suspension period without building a new architecture. For industrialists, this translates into an intermediate environment: part of Ga-Ge flows remains outside the effective scope, but under a latent regulatory threat less than twelve months away.

II. Implementation Schedule and Strategic Suspensions

A. Chronology of Announcements and Suspensions

Since the autumn of 2025, the regulatory trajectory has been organized in short sequences, with structuring announcements followed by partial suspensions. The following table summarizes the major milestones communicated in the cited sources:

| Date | Announcement | Content | Current Status |

| October 9, 2025 | Announcements 55, 58, 61, 62 | Extended controls on rare earths, advanced semiconductors, processing technologies | Suspended until November 10, 2026 [2][3] |

| October 30, 2025 | Pre-suspension | MOFCOM suspends implementation of October 9 measures for one year | In effect [7] |

| November 5, 2025 | Announcement 72 (Partial) | Suspension of U.S.-specific restrictions on gallium, germanium, antimony, and super-hard materials | In effect until November 27, 2026 [3][6] |

| November 9, 2025 | Announcement 72 (Full) | Suspension of Article 2 of Announcement 46 (2024), restoring standard licensing channels for U.S. civilian customers | In effect until November 27, 2026 [3][6] |

Two dates emerge as distinct pivots for the operational management of Ga-Ge flows:

- November 27, 2026: End of the suspension of restrictions specifically targeting gallium and germanium flows to the United States (possible reactivation of Announcement 46 effects for U.S. civilian customers) [6];

- November 10, 2026: End of the suspension of Announcements 55, 58, 61, 62, which would pave the way for full activation of extraterritorial obligations [2][3].

This temporal asymmetry creates a period of approximately ten months where the dominant question is not the physical availability of Ga/Ge, but the anticipated trajectory of controls and the capacity of supply chains to absorb a potential regulatory regime change without operational rupture.

B. From Ban Regime to Standard Licensing Regime

Before November 2025, Announcement 46 (2024) instituted a principle-based ban striking re-exports of gallium and germanium to U.S. civilian customers [2]. The filter was then binary: flows authorized to certain countries and segments, flows structurally blocked to others. The sequence opened by Announcement 72 substituted this logic of prohibition with a standard licensing regime, returning to ordinary examination channels for U.S. civilian users [3].

Operational Example. A German distributor re-exporting Chinese-origin gallium wafers to a civilian semiconductor manufacturer established in the United States was previously blocked by Clause 2 of Announcement 46. Since November 2025, the same operation is theoretically possible subject to obtaining a standard license, the outcome no longer being decided by an automatic ban but by the evaluation of the application by the Chinese authority [2].

This change does not eliminate risk; it modifies its form. The critical point becomes the management of license queues, calendar uncertainties, and potential selective hardening for certain categories of users or uses. The architecture allows the Chinese regulator to adjust pressure on Ga-Ge flows at a much finer rhythm than a frontal ban permitted.

III. Operational Implications: Supply Chain Friction and Compliance Burdens

A. Lengthening Lead Times and Regulatory Uncertainty

Licenses are becoming the new operational unit of measurement for Chinese-origin Ga-Ge flows. Available sources do not precisely document average lead times for licenses targeting gallium and germanium. Nevertheless, the general Chinese regime for dual-use goods mentions review ranges on the order of several weeks, which can extend when the end-user or end-use justifies reinforced examination [4].

Added to this temporal layer is the uncertainty linked to suspensions: the environment of January 2026 relies on transitional regimes expiring in November 2026. Chinese authorities insist in their communications on the legal and non-discretionary nature of export controls, while retaining the possibility of reactivating stricter measures at the end of suspensions [6]. For value chains, the direct consequence is the multiplication of scenarios to manage in parallel: continuity of the standard licensing regime, return to a more restrictive regime, or full activation of extraterritorial mechanisms.

B. Civil/Military Segmentation and End-User Verification

The Ga-Ge regime relies on strict segmentation between civilian and military supply chains, which reverberates down to intermediate distribution levels [1][3]. This segmentation is not merely a contract clause; it implies evidentiary mechanisms and technical filtering tools.

Exporters are required to obtain end-user certifications detailing the intended use and confirming the absence of military destination or link with a military user [1]. These certifications must be cross-referenced with Chinese export control lists and watch lists, including subsidiaries, branches, and entities owned at least 50% by restricted entities [1]. The mechanism thus creates an expanded Know-Your-Customer (KYC) obligation, where diligence is not limited to the direct client but extends to the capital ownership chain.

For U.S. civilian semiconductor manufacturers, this architecture translates into increasingly granular documentation requirements: end-use declarations, shareholding charts, proof of non-indirect military use. On the side of Chinese exporters and distributors in hubs such as Germany or Singapore, downstream end-user verification becomes a structural function of sales management. Each lot of gallium or germanium thus acquires a documentary dimension that adds to its physico-chemical characteristics.

C. Extraterritorial Obligations and Logistics Friction

Even suspended in the short term, Announcement 61 already functions as a strong signal for non-Chinese industrial structures. It introduces the concept that a lot of Chinese-origin Ga/Ge retains a “regulatory footprint” throughout its life, including after multiple stages of processing and successive re-exports [3][5].

An illustrative scenario often cited in analysis involves a semiconductor manufacturer based in Taiwan, using Chinese-origin gallium to produce GaN wafers destined for U.S. civilian clients. If Announcement 61 is fully activated after November 2026, this manufacturer could be required to obtain an export license from MOFCOM to ship its wafers to the United States [5]. Such an obligation would imply not only collecting origin data on inputs but also documenting processing methods and implementing traceability registers compatible with Chinese requirements.

This dynamic adds an extra dimension to logistics: beyond the choice of maritime or air route, assembly hub, or transport schedule, the question becomes whether an operation triggers a licensing requirement from a foreign authority. Non-compliance, when requirements apply, theoretically exposes companies to penalties potentially reaching a significant multiple of the turnover associated with the concerned transactions [5], turning a punctual compliance incident into a business continuity risk.

D. Distribution Channel Segmentation and Logistics Routing

Faced with this complexity, Ga-Ge chain actors tend to structure distinct distribution channels according to client profiles and the regulatory origin of the material. Flows incorporating Chinese gallium or germanium destined for verified civilian users follow a channel subject to specific regulatory scrutiny (MOFCOM licenses, end-user verification, usage documentation). Flows targeting more sensitive segments, including military or dual-use clients, refocus on non-Chinese sources, when these are available at the required scale.

An often-underestimated consequence lies in the progressive rigidification of distribution networks. Channels calibrated for Chinese compliance become harder to rapidly reconfigure in case of a sudden framework change. This organizational inertia transforms regulatory decisions with a one-year horizon into multi-year structural constraints for value chains.

IV. Compliance Framework: Supplier Evaluation and Risk Management

A. Compliance Prerequisites for Chinese Exporters

Chinese authorities encourage the implementation of robust internal control systems at exporters. In the case of gallium and germanium, these Internal Compliance Programs (ICPs) generally include:

- Detailed product classification based on control codes and forms (metal, ingot, wafer, compound);

- Systematic verification procedures for end-users and declared uses;

- Designation of compliance officers with sufficient autonomy to block a doubtful transaction;

- Documentation retention protocols (contracts, end-user certificates) for durations compatible with regulatory requirements.

Exporters who demonstrate effective functioning of these systems generally benefit from greater predictability. Conversely, recurrent failings can lead to increased surveillance. In a context where the Ga-Ge regime is likely to tighten after November 2026, the quality of these internal programs becomes a determining resilience factor for Chinese groups active in these metals.

B. Foreign Buyer Diligence and Supplier Qualification

Companies located outside China relying on Chinese-origin Ga-Ge inputs find themselves, de facto, drawn into the scope of these mechanisms. Supplier qualification must now include:

- The supplier’s capacity to recurrently obtain Ga-Ge licenses for targeted user profiles;

- Transparency regarding input origin and technologies used in critical stages;

- Robustness of internal filtering procedures to prevent downstream clients from triggering ex-post re-evaluations;

- Compatibility between contractual business continuity commitments and the reality of Chinese licensing constraints.

C. Articulation with U.S., European, and Allied Regimes

The Chinese Ga-Ge regime interferes with other frameworks, notably U.S. controls on advanced semiconductors and EU dual-use regimes. This layering creates areas of overlap where a single flow may require sequential licenses in multiple jurisdictions.

The surprising element highlighted by recent flow analysis is that the bottleneck is not always where expected: some segments see the main constraint shift from U.S. control to Chinese control, or vice versa, depending on product form and final destination. In this context, coordination capabilities between legal teams, operational functions, and logistics partners become a major determinant of industrial continuity.

V. Industrial Scenarios and Potential Trajectories for the Ga-Ge Regime

Looking toward the November 2026 deadlines, several regulatory trajectories remain open, each entailing a distinct operational risk profile.

A. Scenario: Maintenance of Standard Licensing Regime

In a continuity scenario, current suspensions would be extended. Such an environment would consolidate a landscape where the main risk is not a brutal supply cut, but dependence on sometimes opaque administrative processes. The value chain would remain under documentary pressure but gain in planning horizon, favoring configurations where refining remains partially anchored in China.

B. Scenario: Reactivation of Reinforced Restrictions toward the U.S.

If suspensions targeting the U.S. are not extended, standard licenses would become more difficult to obtain. Flows to the United States would have to be reconfigured toward non-Chinese inputs, leading to punctual congestion phenomena at alternative producers and lengthened material qualification times.

C. Scenario: Full Activation of Extraterritorial Obligations (Announcement 61)

Full activation of Announcement 61 would introduce a new layer of risk: Ga-Ge processing sites outside China would themselves become Chinese law compliance nodes. Industrial localization decisions would be strongly influenced by a site’s capacity to manage direct relations with the Chinese regulator. This scenario would redefine the role of current industrial hubs, potentially favoring “out-of-scope” clusters for materials not marked by Chinese origin.

D. Second-Order Effects and Map Reconfiguration

Several underlying trends are already emerging:

- Progressive ramp-up of Ga-Ge refining capacities outside China;

- Multiplication of long-term contracts integrating clauses on regulatory origin;

- Increased attention to gallium and germanium recyclability as a lever to reduce exposure to primary controls;

- Clearer differentiation between market segments “tolerant to regulatory risk” and “intolerant” segments (critical infrastructure, defense), with increasingly distinct value chains.

VI. Conclusion: The Structural Weaponization of Complexity

The Gallium-Germanium licensing regime is not a temporary trade dispute; it is the pilot program for a new era of economic statecraft. China has successfully demonstrated that it does not need to embargo a resource to control it. By shifting from restriction of volume to restriction of information (end-user transparency), Beijing has effectively annexed the compliance departments of Western high-tech firms.

The current suspension until November 2026 is likely not a retreat, but a data-gathering phase. By forcing companies to apply for licenses, the regulator maps the exact dependency of the global semiconductor and optical value chains. When the suspension lifts, the controls can be reapplied with surgical precision, targeting specific nodes rather than broad sectors.

The Strategic Verdict:

The era of the “neutral commodity” is over. For the next decade, supply chain resilience will not be defined by access to metal, but by the segregation of flows. Industrial actors face an inevitable bifurcation:

- A “China-Compliant” Chain: Low-cost, high-volume, but transparent to Beijing and vulnerable to sudden political leverage.

- A “Sovereign” Chain: Higher-cost, lower-volume, non-Chinese origin, essential for defense and critical infrastructure.

Attempting to blend these two worlds is the single greatest operational risk for 2026. The winners will not be those who find the cheapest gallium, but those who can prove—document by document—that their supply chain has picked a side.

Note on TI22 Methodology

This analysis relies on the systematic cross-referencing of public regulatory texts (including MOFCOM announcements), open data on gallium and germanium flows, and technical reading of end-use specifications in semiconductors, optronics, and critical infrastructure. This triangulation aims to directly link legal developments to operational failure modes observable in the field. It is continuously updated as new regulatory and industrial signals emerge.

Sources & References

Sources & References

[1] Fastmarkets – China suspends export prohibition on superhard materials to US

[2] ChemRadar – Analysis of China’s export control announcements on gallium, germanium and related materials

[3] Mining.com – China lifts export ban on gallium, germanium and antimony to US

[4] CIRS Group – Export control update on gallium, germanium, ultra-hard materials and graphite

[5] CSIS – Beyond Rare Earths: China’s Growing Threat to Gallium Supply Chains

[6] GVW – China export control update on gallium, germanium and related products

[7] Clark Hill – China hits pause on rare earth export controls and what it means for supply chains