Lithium has flipped in a short period from headlines about scarcity and price spikes to talk of glut and “winter” for battery metals. For supply, procurement and compliance teams, the concern is less the label on the cycle and more the combination of risks: compliance with emerging rules such as the US Inflation Reduction Act (IRA), exposure to a concentrated Chinese refining system, and the practical task of keeping gigafactory build‑outs aligned with secure, auditable raw‑material flows. Several near‑miss episodes since 2022-cargoes stranded in ports, sudden quality downgrades at converters, and delayed audits on origin-have shown that apparent oversupply does not automatically translate into secure or compliant supply.

The working thesis behind this Ti22 briefing is that the current surplus in lithium units coexists with a structural processing choke point. The market looks comfortable on paper, yet a small set of Chinese refiners and policy decisions continues to dictate whether mined spodumene and brines actually become usable, compliant chemicals in the right place and on the right timeline. That combination affects purchasing, governance and supply‑chain strategy at least as much as headline price charts.

Key points at a glance

- The 2023-2025 period is characterised in many analyst datasets by sizeable lithium surpluses and high inventories, keeping battery‑grade prices near multi‑year lows despite ongoing demand growth.

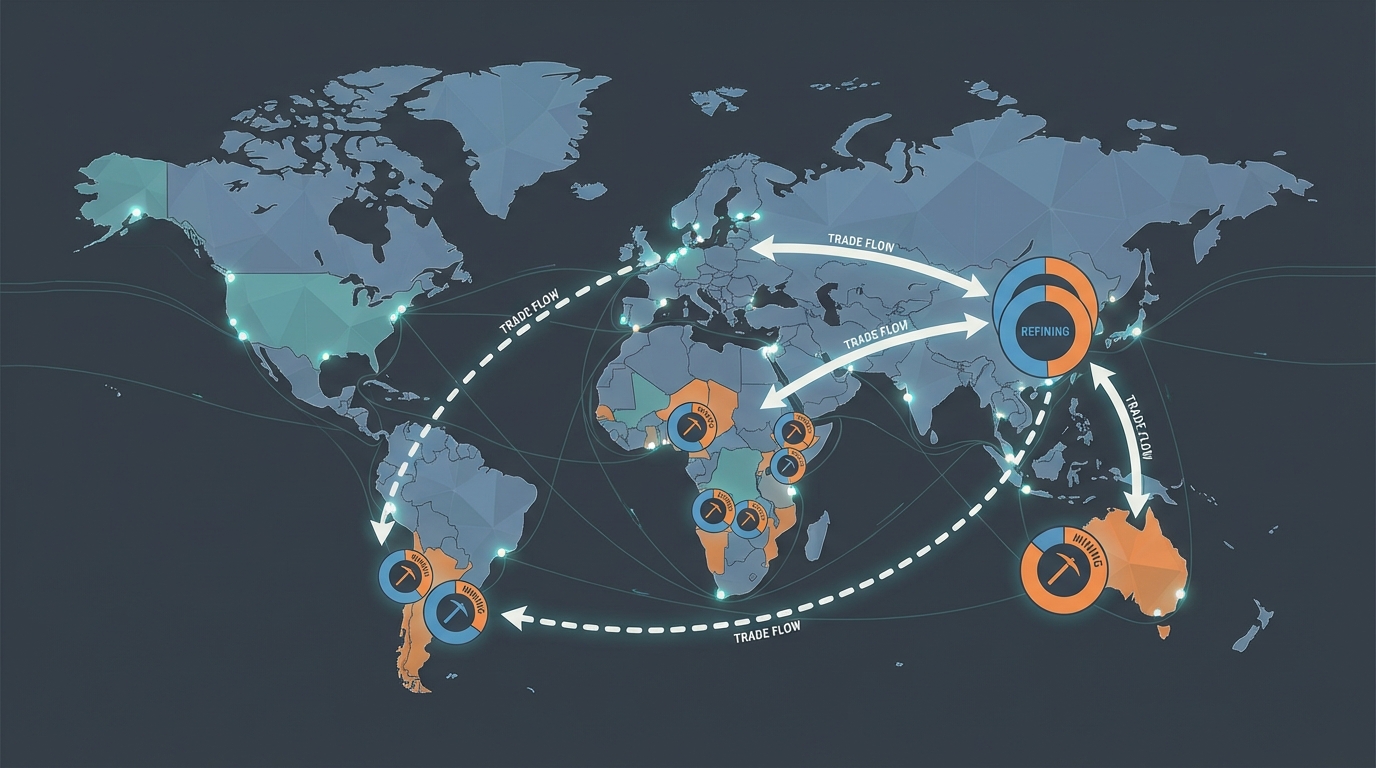

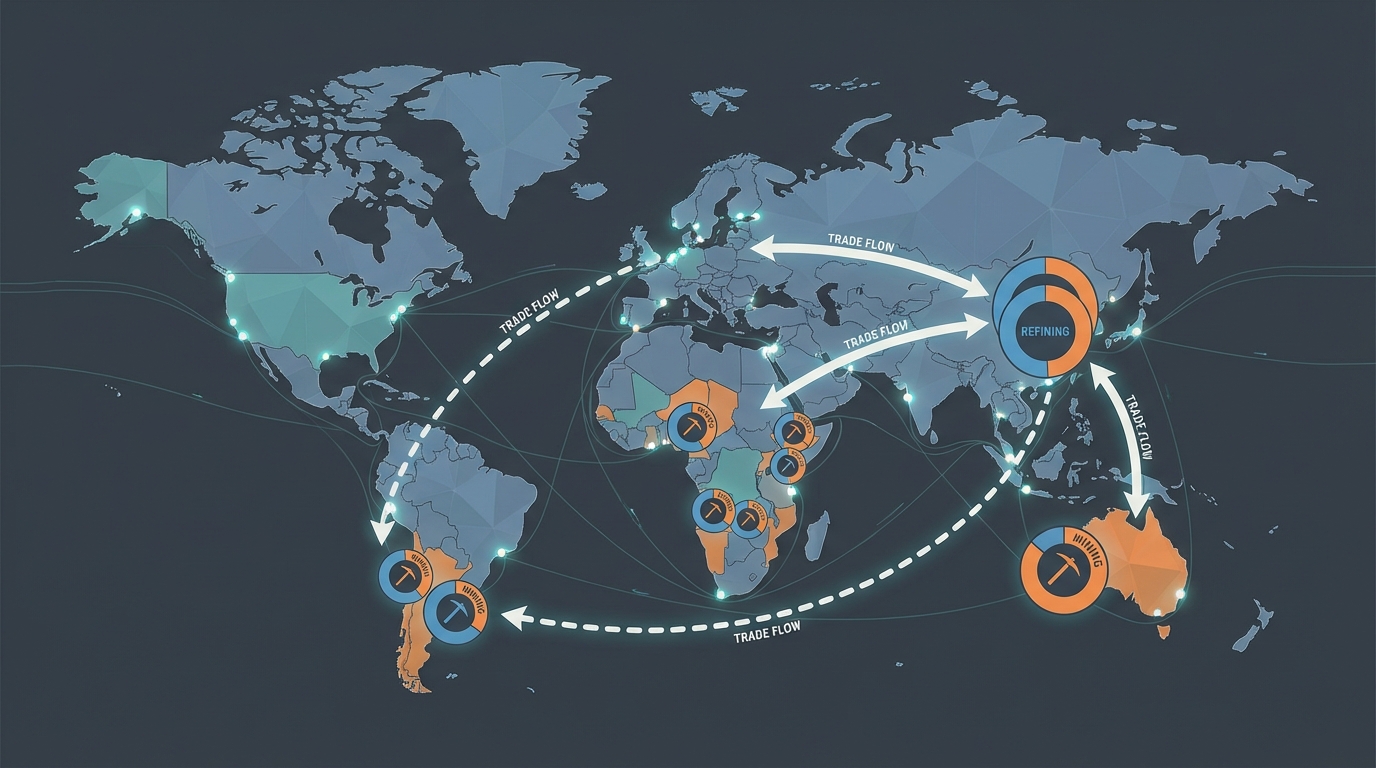

- China is estimated in multiple industry sources to control around 70% of global lithium chemical refining capacity, creating a processing choke point even when mining is geographically more diversified.

- US IRA “foreign entity of concern” (FEOC) rules and allied‑sourcing requirements are pushing a gradual bifurcation between lowest‑cost, China‑centred supply chains and IRA‑compliant chains relying more on US, European and allied production.

- Operationally, this combination translates into tension between short‑term comfort from oversupply and longer‑term concerns about compliance, logistics, refinery concentration and potential policy shifts (for example, Chinese export controls).

- Forecasts referenced in the source deck generally see surpluses narrowing toward the mid‑2020s, with scenarios where modest production cuts or stronger‑than‑expected demand tip the system from loose balance toward deficit.

FACTS: market balance, refining dominance and regulatory perimeter

Supply-demand balance and oversupply narratives

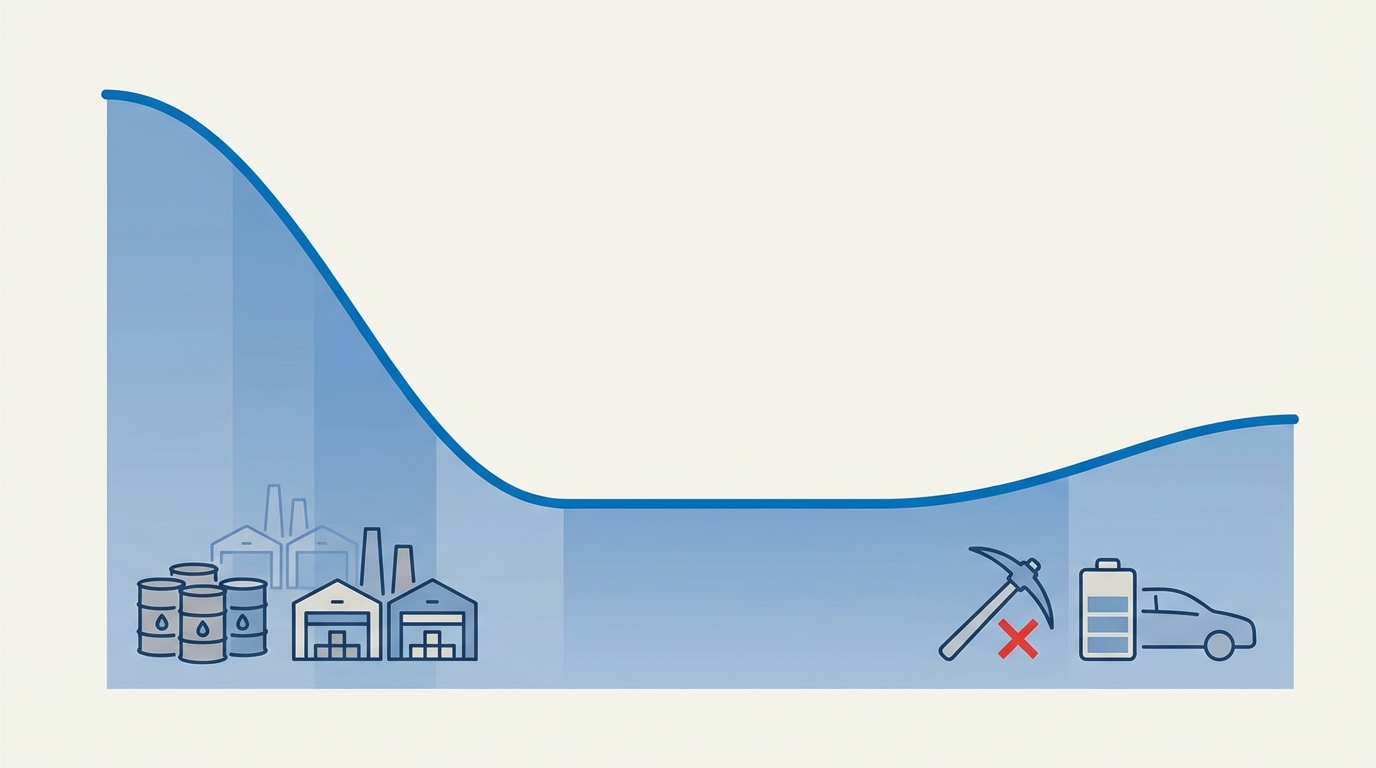

Across the sources cited in the original deck (including Fastmarkets, S&P Global, Macquarie and others), the 2023-2025 lithium market is generally described as being in surplus on an LCE (lithium carbonate equivalent) basis. Several of those forecasts reference surpluses on the order of more than 150,000 tonnes LCE in 2023 and 2024, shrinking to tens of thousands of tonnes in 2025. Exact values differ by institution and by assumptions on recycling and project ramp‑ups, and are inherently uncertain, but the consistent theme is that mined and refined supply grew faster than demand in that window.

Battery‑grade lithium carbonate and hydroxide prices, according to the same sources, fell from the extreme peaks of 2022 to levels around the low five‑figure US‑dollar range per tonne by 2024–2025. Those price points, again differing somewhat between providers, are repeatedly described as being close to the marginal cost for a significant slice of global production. Several analysts cited in the deck argue that at such levels a non‑trivial proportion of higher‑cost mines and brine projects become uneconomic, triggering production curtailments or delays to planned expansions.

Another consistent datapoint in the deck is elevated inventories, particularly in China. Fastmarkets reporting is referenced for port stocks of imported spodumene concentrates on the order of several hundred thousand tonnes, well above earlier norms. The implication is that even if mine output slows, visible stocks can delay any price response and make the market feel looser than underlying mine and refinery decisions would suggest.

On the demand side, cited outlooks from producers and consultancies generally assume continued growth in lithium demand tied to electric vehicles (EVs), stationary storage and other applications. Some of those forecasts describe global lithium demand in 2025 being significantly above 2023 levels and continuing to rise through 2030. Exact numbers vary by scenario, and the deck does not provide a single consolidated demand figure that can be treated as definitive.

China’s refining dominance and market control mechanisms

Multiple independent sources, including the International Energy Agency and industry analysts, have documented that China refines the majority of the world’s lithium chemicals. The deck aligns with that evidence, referencing estimates that roughly 70% of global lithium carbonate and hydroxide production capacity is located in China. That refining capacity processes raw materials mined in Australia, Latin America, Africa and elsewhere into battery‑grade chemicals for both domestic Chinese use and export.

The deck highlights specific companies-such as CATL and Ganfeng—as controlling a significant share of global hydroxide capacity. Exact percentages (for example, “40%+”) are drawn from the cited market commentary and have not been independently recalculated here, but the concentration of refining in a limited set of large Chinese actors is widely recognised.

One example used in the source material is the suspension of mining operations in Yichun, Jiangxi Province, sometimes referred to as the “lithium capital” of China. Environmental and permitting inspections there have, at various points, affected output. The deck describes a specific CATL‑linked mine suspension with a notional capacity of tens of thousands of tonnes LCE per year and associates that with noticeable spot‑price responses. Even without adopting the precise tonnage values provided, the broader point—that operational or regulatory disruptions in a single Chinese refining or mining hub can materially move market pricing and sentiment—has been observable in several episodes since 2022.

The document also references prospective or reported Chinese policy tools, such as anti‑dumping or below‑cost‑sales restrictions on lithium chemicals and the possibility of export licences or quotas modelled on those introduced for gallium and germanium. As of the Ti22 knowledge cut‑off in late 2024, formal Chinese export controls specifically targeting lithium chemicals were a topic of policy discussion rather than a codified regime; any 2025–2026 measures cited in the deck should so be read as reported developments or scenarios from the listed sources, not as independently verified legal text.

US IRA: critical mineral content and FEOC rules

The US Inflation Reduction Act (IRA) introduces several mechanisms that directly affect lithium sourcing, chiefly via: (i) the Clean Vehicle Credit under Internal Revenue Code section 30D; and (ii) the Advanced Manufacturing Production Credit under section 45X. Lithium is in scope as a critical mineral used in EV batteries and energy storage.

Under section 30D as implemented by Treasury and the IRS, eligibility for the clean vehicle tax credit is conditioned on minimum percentages of the value of critical minerals in the battery being extracted or processed in the United States or in countries that have a free trade agreement (FTA) with the US, or recycled in North America. These minimum percentages increase over time. In addition, starting with specified phase‑in dates, batteries are ineligible if any applicable critical mineral or battery component is sourced from a “foreign entity of concern” (FEOC), a term that includes certain entities connected to China, Russia, Iran and North Korea under statutory and regulatory criteria.

The FEOC regime itself uses a 25% threshold in defining when an entity is considered foreign‑entity‑of‑concern controlled, based on ownership interests and board participation criteria. That 25% threshold relates to control tests for entities, not directly to a simple percentage of “Chinese content” in a given battery. The practical effect, however, is that lithium chemicals extracted, processed or recycled by FEOCs can disqualify a vehicle from the credit once the relevant provisions are fully in force.

Section 45X provides a production tax credit for certain domestic manufacturing activities, including the production of critical minerals and battery components. Treasury guidance sets out how lithium chemicals produced in the US or certain allied jurisdictions can qualify. The deck alludes to specific dollar‑per‑unit credit amounts for cathodes and other components, as well as rising localisation thresholds over time. These values are drawn from US guidance but also from analyst interpretation, and are subject to future regulatory updates.

Several sources cited in the deck forecast that a large share of lithium used in US‑bound LFP (lithium iron phosphate) and other batteries in the mid‑2020s would initially be processed in China, creating a tension between commercial sourcing patterns and IRA compliance. Exact estimates of the percentage of US‑bound batteries relying on Chinese refining, or of the total value of credits at risk, differ between analysts and cannot be treated as precise aggregates here.

European and other regulatory initiatives

On the European side, the EU’s Critical Raw Materials Act (CRMA) sets non‑binding benchmarks for domestic extraction, processing and recycling of critical raw materials, including lithium, by 2030, as well as diversification targets intended to limit dependence on any single third country. Environmental permitting and local opposition have nevertheless delayed or constrained several European lithium projects, such as proposed mines in Serbia and Portugal referenced in the deck.

Other jurisdictions, including Canada, Australia and several Latin American states, have updated or proposed frameworks around foreign ownership, national interest tests, water use and downstream processing for lithium projects. The detailed provisions vary by country and are not exhaustively listed in the deck, but collectively they form part of the regulatory environment in which supply‑chain decisions on mine selection, refining location and long‑term partnerships are made.

Analyst price and balance projections

The source material compiles a range of analyst and industry projections for lithium prices and balances through 2026 and beyond. Examples include:

- Forecasts in which battery‑grade lithium carbonate prices stabilise or modestly recover from 2024 lows into the 2025–2026 period, with indicative ranges cited in the low‑ to mid‑five‑figure US‑dollar per tonne zone.

- Scenarios from Fastmarkets and others where the global lithium market moves from substantial surplus in 2023–2024 to a smaller surplus in 2025 and potentially to deficit by 2026, depending on project delays and demand realisations.

- Producer and consultancy views that see lithium demand roughly doubling between the mid‑2020s and 2030 under base‑case EV and storage adoption pathways.

All such forecasts are inherently uncertain and are sensitive to assumptions on EV subsidies, battery chemistry choices, technological shifts (such as increased sodium‑ion adoption), project execution, permitting and macroeconomic conditions. They are included here as reference points from the publicly cited sources in the deck, not as Ti22 projections.

INTERPRETATION: structural choke points, trade‑offs and operational consequences

From “glut” to processing chokehold

The most forceful argument in the deck is encapsulated in the line: “This glut is no cycle repeat—it’s a refining chokehold.” From a supply‑chain and governance standpoint, that framing is compelling. If lithium is thought of purely as a mined commodity, surplus tonnage and lower prices look like unambiguous relief. Once the processing layer and regulatory overlay are brought in, the picture becomes more complicated.

Insofar as approximately 70% of refining capacity is concentrated in one country, even a globally comfortable balance of mined ore and brine can coexist with local bottlenecks, sudden regulatory interventions and quality constraints at a small number of Chinese converters. Case studies from the 2022–2023 period already showed how a temporary shutdown or environmental inspection at a single refining cluster could ripple through cathode plants and cell manufacturing schedules. When compliance with IRA or similar rules is layered on top, the notion of “fungible” lithium units breaks down; specific parcels must meet origin, processing and traceability tests that generic surplus figures do not capture.

For organisations with strict security‑of‑supply standards, this implies that a spot‑market strategy anchored purely on headline surplus indicators is structurally fragile. Operational resilience depends not only on whether there is enough lithium in aggregate, but on whether there is dependable access—over several years—to refining routes and jurisdictions compatible with regulatory and internal‑governance constraints.

IRA‑driven bifurcation of supply chains

The IRA’s FEOC and localisation rules are already nudging the lithium value chain toward a two‑track structure:

- One track remains heavily centred on Chinese refining, prioritising scale, existing infrastructure and historically lower processing costs, and predominantly serving markets or product segments less constrained by IRA‑style rules.

- A second track seeks IRA‑compliant pathways, emphasising extraction, processing and recycling in the US and allied jurisdictions, often at higher initial cost and with tighter capacity constraints but with lower policy and audit risk under current US rules.

In practice, many OEMs and cell manufacturers appear to be running hybrids of these two tracks, with different supply streams feeding different product lines or geographies. That architecture is operationally complex: it requires granular traceability, contractual clarity on origin and processing steps, and governance structures capable of arbitrating between commercial attractiveness and policy compliance.

The deck’s suggestion that Western refining capacity in the mid‑2020s remains insufficient to cover all IRA‑eligible demand is consistent with project pipelines visible in 2024. Numerous refinery projects in North America, Europe and allied countries have been announced, but many remain under construction or in ramp‑up, and not all will deliver nameplate output on schedule. Until those units are online and qualified, a meaningful fraction of lithium‑containing products aimed at global markets will continue to run through Chinese refineries, regardless of surplus or deficit at the mined‑ore level.

Risk pathways observed in purchasing and governance

Across procurement reviews and supply‑chain case studies that Ti22 has examined, several recurring risk pathways emerge in the current lithium environment:

- Compliance lag versus physical flow. Physical flows of lithium chemicals were often shifted quicker than compliance and traceability systems could adapt, leading to situations where material technically met specifications but could not be cleanly allocated to an IRA‑eligible or CRMA‑aligned product line.

- Refinery concentration risk. A tendency to focus diversification efforts at the mine level, while leaving a high degree of concentration in a narrow set of Chinese converters and tollers, created hidden single points of failure in processing.

- Inventory and valuation exposure. In an oversupplied market, building large inventories felt prudent from a security‑of‑supply standpoint, but when price benchmarks fell further, board‑level scrutiny shifted to write‑downs and working‑capital drag. This tension is particularly acute for entities carrying strategic stockpiles.

- Logistics and chokepoint stacking. Episodes such as Red Sea shipping disruptions showed how freight bottlenecks can stack on top of refining concentration, amplifying delays and uncertainty even when upstream mines are operating normally.

None of these patterns are unique to lithium; similar dynamics have appeared in cobalt, rare earths and other critical minerals. What stands out in lithium is the pace of demand growth and the scale of announced downstream investment, which compress the timeline available for operational learning and adjustment.

How production cuts and project delays might tighten balances

The deck lists a range of announced or discussed production cuts, mine suspensions and project deferrals—such as curtailments at higher‑cost brine operations in Argentina or delayed expansions in Australia—as well as environmental‑driven slowdowns in Chinese hubs like Yichun. If a significant portion of those curtailments persists while EV and storage demand continue to expand broadly in line with the more conservative forecasts, the market could shift from a clear surplus toward a more balanced or even tight condition by the mid‑ to late‑2020s.

However, any projection of a structural deficit by a particular year rests on assumptions that deserve explicit caveats. Among the key uncertainties:

- EV adoption could under‑ or overshoot current expectations, especially in Europe and China where policy support is evolving.

- Non‑lithium chemistries (for example, sodium‑ion) could take a larger share in certain segments, moderating lithium demand growth.

- Technological shifts such as higher recovery rates, direct lithium extraction (DLE) or increased recycling could add incremental supply relative to today’s baselines.

- Conversely, community opposition, water‑use restrictions or permitting hurdles could delay or cancel individual projects that are currently assumed to be online by 2026–2030.

Because these variables interact, scenario analysis rather than point forecasts is the more robust way to think about mid‑decade tightness. The direction of travel—that large surpluses are unlikely to persist indefinitely if demand growth continues and weaker producers curtail—is broadly accepted. The exact timing and severity of any tightening remains uncertain.

Implications for security of supply and internal governance

In boardrooms and risk committees, lithium now sits in an uncomfortable space: no longer an obscure line item, but not yet a stable, commoditised input like iron ore. Security‑of‑supply questions are being asked in the same breath as environmental, social and governance (ESG) and compliance questions. Typical points of pressure include:

- Traceability and audit readiness. IRA and similar rules effectively require credible chain‑of‑custody data on lithium origin and processing. Systems built for bulk commodities often struggle to provide this granularity at scale, particularly when feedstock is blended.

- Policy risk concentration. Heavy reliance on Chinese refiners exposes supply chains to policy decisions—export licensing, environmental enforcement, informal guidance on minimum pricing—that fall outside the commercial parties’ control.

- Capital allocation under uncertainty. Investments in Western refining or joint ventures can enhance compliance and diversification, but they lock in capital based on regulatory frameworks that may evolve. Boards confront the trade‑off between moving early and waiting for additional clarity.

An important shift over the last two years has been the move from treating regulatory compliance as a retrofit on top of commercial decisions, to integrating it into upfront sourcing, qualification and partnership discussions. Where that integration is incomplete, frictions are now visible in delayed product launches, requalification cycles and complex renegotiations with suppliers.

WHAT TO WATCH: indicators and weak signals

Several categories of indicators merit continuous monitoring, as they will shape how the lithium landscape evolves from a perceived surplus toward tighter or more structurally diversified conditions:

- US regulatory guidance updates. Further IRS/Treasury clarifications on FEOC definitions, look‑through rules for joint ventures, and documentation requirements for 30D and 45X claims will directly affect which lithium flows can credibly underpin credit‑eligible products.

- Chinese policy moves. Any formal introduction of export licences, quotas or below‑cost‑sales restrictions for lithium chemicals—analogous to measures seen in gallium and germanium—would immediately change the risk calculus around reliance on Chinese refiners.

- Commissioning and ramp‑up of non‑Chinese refining. Milestones at projects in Australia, Europe, North America and Latin America (including brine‑to‑hydroxide and DLE pilots) will indicate whether the world is on track to dilute China’s refining share or whether dependence remains entrenched.

- EV and storage deployment data. Actual sales and installation numbers, particularly in Europe and China, will validate or challenge current demand forecasts and hence the timing of any move from surplus to balance or deficit.

- Inventory and port‑stock trends. Changes in Chinese port inventories of spodumene and in reported stocks of lithium chemicals offer early clues on whether apparent oversupply is being drawn down or entrenched.

- Project permitting outcomes. Decisions on high‑profile projects in Europe, North America and Latin America—positive or negative—will shift the medium‑term supply outlook and signal how environmental and social concerns are being balanced against strategic‑materials policies.

From a supply‑chain governance perspective, these signals matter not only individually but in combination: for example, a tightening of US FEOC guidance at the same time as a new Chinese export licensing regime would have very different implications than either move in isolation.

Note sur la méthodologie TI22 Cette analyse croise la surveillance continue des textes et projets de textes des principales autorités (États‑Unis, Union européenne, Chine et pays producteurs clés), les éléments de marché publiés dans les sources listées dans le deck d’origine, et l’examen des spécifications techniques des usages finaux (batteries EV, stockage stationnaire, applications de défense). Les chiffres de marché et projections de prix mentionnés restent ceux des sources citées et ne constituent pas des estimations internes de TI22.

Conclusion

The lithium market of 2025 is marked by an unusual juxtaposition: comfortable aggregate balances and low prices on many analyst charts, alongside a structurally concentrated refining system and tightening regulatory constraints on origin and processing. For operational teams, the resulting environment is less about choosing between “bearish” and “bullish” views and more about managing layered risks—processing bottlenecks, policy shifts, compliance audits and logistics shocks—within existing budgets and project timelines.

Analyst projections in the public domain suggest that current surpluses may narrow as higher‑cost production is curtailed and demand continues to grow, but the pace and timing of any tightening remain uncertain and highly path‑dependent. In that context, governance frameworks that treat lithium as a strategic input—integrating regulatory, technical and supply‑risk perspectives—appear better aligned with the realities of this market than approaches that focus solely on short‑term price cycles. Whatever path the market ultimately takes, active monitoring of weak regulatory and industrial signals will be central in shaping informed, compliant and resilient supply‑chain decisions.

Sources

- Lithium Prices Hit 5-Year Low as Oversupply Persists — reuters.com

- China Tightens Grip on Global Lithium Refining Amid Price Collapse — bloomberg.com

- Lithium’s Boom-to-Bust Cycle and the Challenge of Chinese Refining Control — ft.com

- Global Lithium Oversupply Widens in 2025 as Demand Slows — mining.com

- China’s Lithium Chemical Dominance Leaves Global Supply Imbalanced — asia.nikkei.com

- Global Lithium Market Outlook 2025 — iea.org

- Inflation Reduction Act ‘Foreign Entity’ Rules Hit Battery Supply Chains — politico.com

- Chinese Refineries Hold 70% of Global Lithium Capacity, Report Finds — spglobal.com

- Lithium Oversupply and IRA Compliance Risks in 2025 — supplychaindive.com

- Lithium Market 2025: Oversupply and Refining Bottleneck Outlook — benchmarkminerals.com